The impending rule changes by the Consumer Federal Protection Bureau (CFPB) will not only dramatically affect the way Americans buy and sell real estate, but also how lenders, realtors, attorneys and title professionals do business. Northbrook, Ill-based Proper Title, LLC, a full-service title insurance agency serving the residential and commercial real estate industries, breaks down what homebuyers and industry providers need to understand, and how to prepare for the changes taking effect on August 1, 2015.

1. Everyone at the closing table will be affected

The CFPB rule changes will improve the content and delivery of information for consumers through the addition of online estimating tools, clearer language to describe associated fees, defined review periods, and a simplified number of documents needed for each transaction. “The new rules apply to all purchases of residential property, including refinancing, purchasing vacant land, construction-only loans, and even timeshares,” said Ben Niernberg, executive vice president of business development and operations at Proper Title. “Among the few exceptions are all-cash purchases, reverse mortgages and home equity lines of credit, so you can see, it still touches the majority of transactions.”

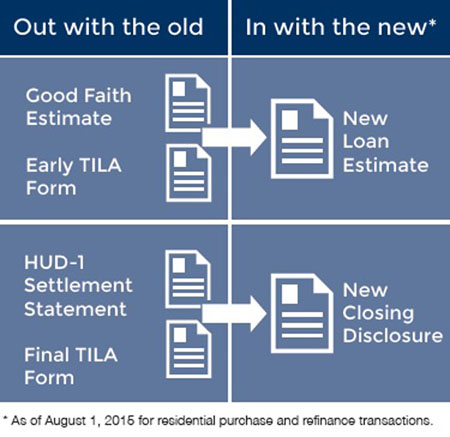

The current forms and processes under the Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) will be consolidated and enhanced under the new rules. Rather than two disclosure forms when applying for a mortgage, followed by two additional forms before the closing, the new rules will require a total of just two forms.

“While this simplifies the process from a consumer’s perspective, it requires a substantial amount of front-end work on the part of providers to update the systems and materials they rely on for every transaction,” said Niernberg. “And beyond system integration, providers, particularly brokers and attorneys, will need to understand the new requirements so they can properly inform their clients.”

The consolidated forms consist of the current Good Faith Estimate (GFE) and early Truth-in-Lending Act (TILA) forms, which will be replaced with the new Loan Estimate that will also include a summary of loan terms and an estimate of loan and closing costs. The current HUD-1 Settlement Statement and final TILA form will also be replaced with the new Closing Disclosure.

“Purchasing real estate has changed dramatically over the past few years, but the current forms and requirements have been in place for over three decades,” said Niernberg. “The time is right for these changes to be implemented.”

2. Closing on a property will take longer

In addition to simplifying the forms, the CFPB is instituting review periods to help ensure consumers understand the details of their transaction. “Sellers who are anxious to sell and buyers who are trying to coordinate their move-in date, will need to consider the new application and review periods and plan accordingly,” said Niernberg.

Borrowers will have three days to review the new five-page Closing Disclosure form. ”It’s important to note that there is a three-day period for receipt of the Closing Disclosure, and only after receipt has been confirmed, the three-day review period begins counting down. Niernberg explained. “That can push the closing six days out, but we’re talking about business days, so if it falls on a weekend, it could be even longer.”

He added, “However, if changes are required, there are limits to the reasons a closing could be further postponed. It can only be delayed if the APR increased by more than an eighth of a percent, if it changes from a fixed-rate to a variable-rate, or if any prepayment penalties are applied. It cannot be delayed for other reasons, like problems during the walk-through.”

The Closing Disclosure not only lists the many terms and provisions of the loan, but also a detailed estimate of the closing costs. “When you consider the amount of financial information contained in this single form, preparation of the Closing Disclosure will take a collaborative effort between lenders, settlement companies and other vendors,” said Niernberg. “It’s critical that each provider executes his or her role in a timely manner to avoid needless delays for the consumer.”

3. Lenders, Realtors, attorneys, and title insurance agencies need to be ready by August 1, 2015

In addition to integrating its systems with the new forms and rate calculators, Proper Title has been hosting free educational seminars available to brokers, attorneys, and lenders, outlining the requirements of the rule changes. The sessions are also eligible for continuing education credits.

“Although we’ve known since 2013 that these changes were coming, many industry professionals have not fully updated their systems,” said Niernberg. “Integrating the new required fee quotes, generating the new closing disclosure forms, and implementing tracking systems to gauge the delivery and waiting periods is no small undertaking. But the first step is to understand exactly what has changed, and that involves everyone from the broker, to the lender, to the attorney.”

For title insurance providers, the Closing Disclosure will bring significant changes in how information is presented to sellers and buyers. For example, any applicable discounts for buying multiple policies must be itemized – but without noting the discounted rates. “We’ve always understood how critical it is that home sellers and borrowers fully understand the fees and what’s an appropriate rate,” said Niernberg. “So, for Proper Title, adjusting to the new Closing Disclosure is simply one of logistics, and only fortifies our commitment to clients.”

He added, “The ultimate goal of the CFPB’s rule changes is to protect the consumer. If we as an industry keep the focus on that outcome, we believe it will be a smooth transition and improve the outcome for everyone.”

About Proper Title

Northbrook, Ill.-based Proper Title, LLC, is a full-service title insurance company serving the residential and commercial real estate industries. Since its founding in 2013, Proper Title has become a major player in the industry, on course to be among the top five-largest title insurance agencies in Illinois, and recently earning the “2014 Rising Star / Excellence in Action” award by Fidelity Investments. Proper Title is the first to implement a concierge approach in the delivery of all of its title insurance and escrow services. The concierge approach focuses on every aspect of the process, from dedicating an attorney/broker concierge for each closing to ensure unmatched service, to providing food and beverages, as well as offering multiple device charging stations in each closing room. This unique, service-oriented concept focuses on making the client’s closing experience the best it can be from order to closing. Proper Title also overstaffs in all areas of the closing process to ensure shorter closing times and greater efficiency while maintaining a competitive pricing structure. With eight closing locations in Cook, Lake and DuPage counties, as well as one in New Buffalo, Mich., Proper Title is able to deliver the concierge experience throughout the Chicago area and the Midwest. For more information, visit propertitle.com.

The Consumer Federal Protection Bureau (CFPB) rule changes will consolidate and enhance the current forms for homebuyers. (Photo credit: Fidelity National Title Group)